Since the multiplier for this inventory option is 100, a amount of 1 is similar to trading a hundred shares of TSLA. To sum up, we need to declare an additional 4 parameters compared to a stock contract and we want to use ‘OPT’ because the secType. Here we’ve specified an possibility expiry of October 2, 2020, and a strike worth of $424. There are a few other fields we have to populate to correctly outline an options contract. Interestingly, reqMktData doesn’t return the time the trade occurred, which is the primary cause it wasn’t used in this instance. The reqMktData function sends out tick information each 250 ms (for Stocks and Futures).

The API connection will run in its own thread to ensure that communication to and from the server is not being blocked by different commands in the primary block of the script. IB-insync is a third-party library that utilizes the asyncio library to offer an asynchronous single thread to work together with the API. This may be a solution to explore for those wanting to make use of an interactive environment.

Algorithmic Trading: Definition, The Means It Works, Pros & Cons

We now have a new contract object and we can make a market knowledge request for it by using the same syntax as the prior example. The ReqId is a singular constructive integer you assign to your request which will be included in the response. This method, if you make several market knowledge requests on the identical time, you’ll know which returned knowledge belongs to which asset.

There is a threat, especially with the ‘affected person’ precedence, that through the scanning time the value of the safety might transfer away from the unique worth. The Adaptive Algo is designed to make sure what is api in trading that both market and aggressive restrict orders trade between the bid and ask costs. On common, utilizing the Adaptive algo results in higher fill prices than using regular market or restrict orders.

Algorithmic Buying And Selling

We can reuse most of the code from the sooner part the place we went through an example of firing an order. The reqTickByTickData is extra accurate however will either return the final price or the bid and ask. Lastly, we’ve added a zero.1 second sleep to very briefly pause the script after each examine.

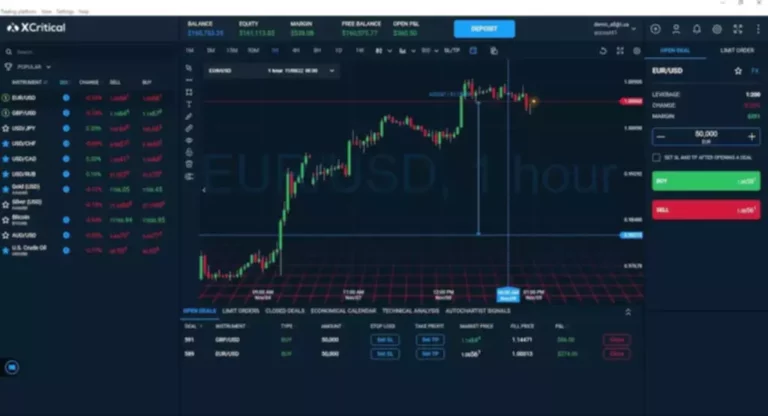

Now click on on the order kind and scroll to IBALGO and select Adaptive within the sidecar window. Select the limit value or select market and click on the Advanced button. In the Algo parameters space “Adaptive” will populate the first drop-down box.

Unlike other algorithms that observe predefined execution guidelines (such as trading at a sure volume or price), black field algorithms are characterised by their goal-oriented strategy. As sophisticated because the algorithms above could be, designers determine the objective and select specific rules and algorithms to get there (trading at sure prices at sure times with a sure volume). Black box systems are completely different since whereas designers set objectives, the algorithms autonomously decide one of the best ways to realize them based mostly on market situations, exterior occasions, etc.

Open Supply Algorithmic Buying And Selling

To get began, get ready with pc hardware, programming expertise, and financial market expertise. However, the practice of algorithmic trading isn’t that straightforward to maintain and execute. Remember, if one investor can place an algo-generated trade, so can other market participants.

Just to ensure it’s put in correctly, go into your Python terminal and type in import ibapi. There are 4 primary steps to establishing a connection to the IB API in Python.

Investments

Nevertheless, it may possibly become troublesome because the API considers the last connection nonetheless lively, and due to this fact won’t permit subsequent connections. The workaround is to alter your client ID but this can become tedious quick. You can lookup https://www.xcritical.in/ legitimate option expiry dates and strikes in TWS both under the OptionTrader or by right-clicking on an asset in your watchlist and clicking on the options icon to pull up a sequence. If you’re following together with this code instance, you may have to change the option expiry if you’re studying this after October 2, 2020.

- These “sniffing algorithms”—used, for example, by a sell-side market maker—have the built-in intelligence to identify the existence of any algorithms on the purchase side of a giant order.

- There are two capabilities to get the up to date contract that options a ConID.

- The tickType, left empty on this example, lets you specify what type of information you’re on the lookout for.

- Usually the market value of the target company is less than the price offered by the buying company.

- Before trading safety futures, read the Security Futures Risk Disclosure Statement.

There are a few special classes of algorithms that try and identify “happenings” on the other facet. These “sniffing algorithms”—used, for example, by a sell-side market maker—have the built-in intelligence to establish the existence of any algorithms on the purchase aspect of a large order. Such detection via algorithms will help the market maker establish massive order opportunities and enable them to profit by filling the orders at a higher price.

When utilizing reqTickByTickData, there’s the potential for several trades coming in quickly with the identical timestamp. This may cause knowledge loss since we’re storing our data based mostly on the time value. It connects to the API, begins a thread, and makes positive a connection is established by checking for the subsequent valid order id. However, we’ve gone over a couple of different order varieties such as bracket orders that include stop-loss ranges or take revenue ranges, and value condition orders. Due to the complexity of order processing, it made more sense to not include it within the class. The only thing completely different here is that we’ve created a dictionary file named bardata.

Such simultaneous execution, if good substitutes are concerned, minimizes capital necessities, but in apply never creates a “self-financing” (free) position, as many sources incorrectly assume following the theory. As lengthy as there is some distinction in the market value and riskiness of the 2 legs, capital must be put up to be able to carry the long-short arbitrage place. Algorithmic buying and selling brings collectively computer software program, and monetary markets to open and close trades based on programmed code. Investors and traders can set when they need trades opened or closed. They can even leverage computing energy to carry out high-frequency trading. With quite lots of strategies traders can use, algorithmic trading is prevalent in financial markets right now.

When the present market value is lower than the typical worth, the stock is considered enticing for purchase, with the expectation that the price will rise. When the present market worth is above the typical value, the market worth is predicted to fall. In different words, deviations from the typical price are expected to revert to the common. Now that we’ve completed our class features, let’s move on to the primary script.